Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

10 Tips to Minimize Stress When Selling Your Home

When I was growing up, my family must have moved a dozen times. After the first few moves, we had it down to a science: timed out, scheduled, down to the last box. Despite our best efforts, plans would change, move-out and move-in days would shift, and the experience would stress the entire family out. Despite the stress, we always managed to settle in our new home and sell our old one before the start of school.

With a lot of planning and scheduling, you can minimize the stress of selling your house and moving. Here are some tips:

Plan Ahead

Know when you want to be moved out and into your new home and have a backup plan in case it falls through. Before you sell your home, familiarize yourself with local and state laws about selling a home so you’re not caught by surprise if you forget something important.

Lists and schedules are going to be your new best friend through the process. Have a timetable for when you want to sell your house when you have appraisers, realtors, movers, etc. over. Also, keep one for when your things need to be packed and when you need to be moved into the new place. I suggest keeping it on an Excel sheet so you can easily update it as the timeline changes (and it will – stuff happens).

Use Resources

First time selling a house? Check out some great resources on what you need to know. US News has excellent, step-by-step guides on what you need to know to sell. Appraisers and realtors can also be good resources, and since you’ll be working with them through the process, be sure to ask them questions or have them point you to resources.

Appraisal

Have your house appraised before you sell so you know your budget for your new home. This will help you look for an affordable home that meets your family’s needs. It will also help you maximize the amount you can receive for your old home. You can also learn useful information from an appraisal, such as which repairs need to be made, if any.

Repairs

Does your house need repairs before you move? If so, figure out whether you’ll be covering them, or whether your buyers will (this will be a part of price negotiations, so factor it in with your home budget). Will you need to make repairs in your new house, or will that be covered? Either way, make sure you know which repairs need to be made – and either be upfront with buyers about them or make them before you sell.

Prepare to Move

If you’re moving to a new town or a new state, you need to prepare more than just a new home. Research doctors and dentists, places to eat, and what to do for fun. If you have school-aged children, look at the local school district or private school options – not only to learn how to enroll your kids, but also to get a feel for the school culture, see what extracurricular activities your kids can do, what standards/learning methods your kids’ new school will implement, etc.

Packing

Think: how soon are you moving, what will you need to use before you move, what can get boxed and what needs to stay out? The sooner you’re moving out, the sooner you need to pack, but if you have time, just take a day per weekend to organize a room, pack what you want to take and arrange to donate what you want to get rid of.

Downsizing

Moves are a great time to purge old, unwanted and unused stuff from your home. Sometimes, it’s necessary if you’re moving into a smaller space. Either way, as you pack each room, think about whether you use what you’re packing to take with you. If you do, pack it to go. If not, put it in a separate box to go to your local donations place. You can also call some organizations to have your unwanted things picked up, no hassle.

If You Have Kids

Moving with kids can be extra stressful. Be sure to include them in the process. This is a wonderful opportunity to teach younger children about moving and prepare them for the changes it brings. Older children can help out with responsibilities, like packing their room or researching their new town.

Your New Place

Moving into a new place takes some planning as well. Once you’ve bought your new home or condo, design at least a basic outline for where your stuff will be set up. Make necessary repairs and decorate (painting, for example) before you unpack. Ideally, you should have some time to do these things before, but if you don’t, don’t be in a hurry to unpack everything – it can be a hassle to paint if you have all your furniture and bookshelves up!

Staying In Touch and Making New Friends

Finally, moving can mean good-byes with family and/or friends. Social media is a great way to keep in touch with people after you’ve moved, but distance can still weaken these old relationships. Make some time to call or message your old friends to keep in touch. Pair that work with a concerted effort to meet new people. See what hobbies or groups are in your new area and start there. It doesn’t seem like a lot, but it can make your new house a home and make your new town a community you can enjoy.

Are You Better Off Paying Your Mortgage Earlier or Investing Your Money?

Photo Credit: Rawpixel via Unsplash

Few topics cause more division among economists than the age-old debate of whether you’re better off paying off your mortgage earlier, or investing that money instead. And there’s a good reason why that debate continues; both sides make compelling arguments.

For many people, their mortgage is the largest expense they will ever incur in their lives. So if given the chance, it only makes logical sense you would want to pay it off as quickly as possible. On the other hand, a mortgage is also the cheapest money you will ever borrow, and it’s generally considered good debt. Any extra money you obtain could be definitely be put to good use elsewhere.

The reality is, however, a little less cut and clear. For some homeowners, paying off their mortgage earlier is the right answer. While for others, it would be far more advantageous to invest their money.

Advantages of paying off your mortgage earlier

- You’ll pay less interest: Each time you make a mortgage payment, a portion is dedicated towards interest, and another towards principal (we’ll ignore other costs for now). Interest is calculated monthly by taking your remaining balance, the length of your amortization period, and the interest rate agreed upon with your lending institution.

If you have a $300,000 mortgage, at a 4% fixed rate over 30 years, your monthly payment would be around $1,432.25. By the time you finish paying off your mortgage, you would have paid a total of $515,609, of which $215,609 were interest.

If you wanted to lower the total amount you pay on interest, you don’t need to make a large lump sum to make a difference. If you were to increase your monthly mortgage payment to $1,632.25 (a $200 a month increase), you would be saving $50,298 in interest, and you’ll pay off your mortgage 6 years and 3 months earlier.

Though this is an oversimplified example, it shows how even a small increase in monthly payments makes a big difference in the long run.

- Every additional dollar towards your principal has a guaranteed return on investment: Every additional payment you make towards your mortgage has a direct effect in lowering the amount you pay in interest. In fact, each additional payment is, in fact, an investment. And unlike stocks, bonds, and other investment vehicles, you are guaranteed to have a return on your investment.

- Enforced discipline: It takes real commitment to invest your money wisely each month instead of spending it elsewhere.

Your monthly mortgage payments are a form of enforced discipline since you know you can’t afford to miss them. It’s far easier to set a higher monthly payment towards your mortgage and stick to it than making regular investments on your own.

Besides, once your home is completely paid off, you can dedicate a larger portion of your income towards investments, your children or grandchildren’s education, or simply cut down on your working hours.

Advantages of investing your money

- A greater return on your investment: The biggest reason why you should invest your money instead comes down to a simple, green truth: there’s more money to be made in investments.

Suppose that instead of dedicating an additional $200 towards your monthly mortgage payment, you decide to invest it in a conservative index fund which tracks S&P 500’s index. You start your investment today with $200 and add an additional $200 each month for the next 30 years. By the end of the term, if the index fund had a modest yield of 5% per year, you will have earned $91,739 in interest, and the total value of your investment would be $163,939.

If you think that 5% per year is a little too optimistic, all we have to do is see the S&P 500 performance between December 2002 and December 2012, which averaged an annual yield of 7.10%.

- A greater level of diversification: Real estate has historically been one of the safest vehicles of investment available, but it’s still subject to market forces and changes in government policies. The forces that affect the stock and bonds markets are not always the same that affect real estate, because the former are subject to their issuer’s economic performance, while property values could change due to local events.

By putting your extra money towards investments, you are diversifying your investment portfolio and spreading out your risk. If you are relying exclusively on the value of your home, you are in essence putting all your eggs in one basket.

- Greater liquidity: Homes are a great investment, but it takes time to sell a home even in the best of circumstances. So if you need emergency funds now, it’s a lot easier to sell stocks and bonds than a home.

Investing In a Green Home Will Pay Dividends In 2019

As we step forward into 2019, eco-friendly “green homes” are more popular than ever. Upgrading your home’s sustainability improves quality of life for those residing in it, but it is also a savvy long-term investment. As green homes become more popular, properties boasting sustainable features have become increasingly desirable targets for homebuyers. Whether designing a new home from scratch or preparing your current home for sale, accentuating a house with environmentally-friendly features can pay big dividends for everyone.

While the added value depends on the location of the home, its age, and whether it’s certified or not, three separate studies all found that newly constructed, Energy Star, or LEED-certified homes typically sell for about nine percent more than comparable, non-certified new homes. Plus, one of those studies discovered that existing homes retrofitted with green technologies, and certified as such, can command a whopping 30-percent sales-price boost.

There are dozens of eco-friendly features that can provide extra value for you as a seller. To name a few:

Cool roof

Cool roofs keep the houses they’re covering as much as 50 to 60 degrees cooler by reflecting the heat of the sun away from the interior, allowing the occupants to stay cooler and save on air-conditioning costs. The most common form is metal roofing. Other options include roof membranes and reflective asphalt shingles.

Fuel cells

Fuel cells may soon offer an all-new source of electricity that would allow you to completely disconnect your home from all other sources of electricity. About the size of a dishwasher, a fuel cell connects to your home’s natural gas line and electrochemically converts methane to electricity. One unit would pack more than enough energy to power your whole home.

For many years, fuel cells have been far too expensive or unreliable. But as technology has improved, so too has reliability. Companies like Home Power Solutions and Redbox Power Systems have increased the reliability of these fuel sources while reducing their size. Much like we’ve seen computers and cell phones shrink in size while improving reliability and power, fuel cells continue to be refined.

Wind turbine

A wind turbine (essentially a propeller spinning atop an 80- to 100-foot pole) collects kinetic energy from the wind and converts it to electricity for your home. And according to the Department of Energy, a small version can slash your electrical bill by 50 to 90 percent.

But before you get too excited, you need to know that the zoning laws in most urban areas don’t allow wind turbines. They’re too tall. The best prospects for this technology are homes located on at least an acre of land, well outside the city limits.

Green roof

Another way to keep the interior of your house cooler—and save on air-conditioning costs—is to replace your traditional roof with a layer of vegetation (typically hardy groundcovers). This is more expensive than a cool roof and requires regular maintenance, but young, environmentally conscious homeowners are very attracted to the concept.

Hybrid heating

Combining a heat pump with a standard furnace to create what’s known as a “hybrid heating system” can save you somewhere between 15 and 35 percent on your heating and cooling bills.

Unlike a gas or oil furnace, a heat pump doesn’t use any fuel. Instead, the coils inside the unit absorb whatever heat exists naturally in the outside air, and distributes it via the same ductwork used by your furnace. When the outside air temperature gets too cold for the heat pump to work, the system switches over to your traditional furnace.

Geothermal heating

Geothermal heating units are like heat pumps, except instead of absorbing heat from the outside air, they absorb the heat in the soil next to your house via coils buried in the ground. The coils can be buried horizontally or, if you don’t have a wide enough yard, they can be buried vertically. While the installation price of a geothermal system can be several times that of a hybrid, air-sourced system, the cost savings on your energy bills can cover the installation costs in five to 10 years.

Solar power

Solar panels capture light energy from the sun and convert it directly into electricity. Similarly to wind turbines, your geographical location may determine the feasibility of these installments. Even on cloudy days, however, solar panels typically produce 10-25% of their maximum energy output. For decades, you may have seen these panels sitting on sunny rooftops all across America. But it’s only recently that this energy-saving option has become truly affordable.

In 2010, installing a solar system on a typical mid-sized house would have set the homeowner back $30,000. But as of December 2018, the average cost after tax credits for solar panel installation was just $13,188! Plus, some companies are now offering to rent solar panels to homeowners (the company retains ownership of the panels and sells the homeowner access to the power at roughly 10 to 15 percent less than they would pay their local utility).

Solar water heaters

Rooftop solar panels can also be used to heat your home’s water. The Environmental Protection Agency estimates that the average homeowner who makes this switch should see their water bills shrink by 50 to 80 percent.

Tax credits/rebates

Many of the innovative solutions summarized above come with big price tags attached. However, federal, state and local rebates/tax credits can often slash those expenses by as much as 50 percent. So before ruling any of these ideas out, take some time to see which incentives you may qualify for at dsireusa.org and the “tax incentives” pages at Energy.Gov.

Regardless of which option you choose, these technologies will help to conserve valuable resources and reduce your monthly utility expenses. Just as importantly, they will also add resale value that you can leverage whenever you decide it’s time to sell and move on to a new home.

by John Trupin, Windermere

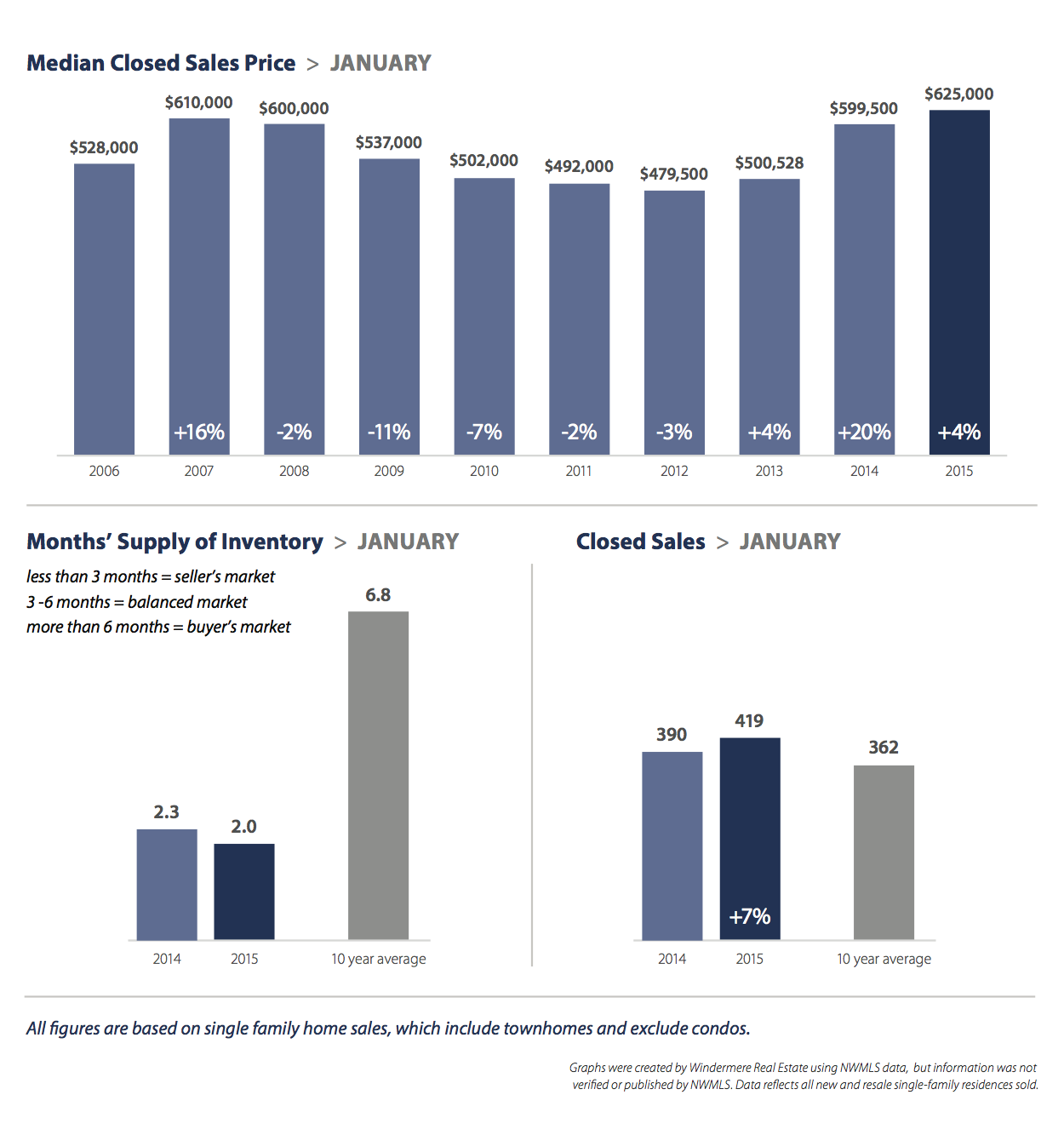

Neighborhood Update – February 2015

The new year started out with a bang. The market saw year-over-year increases in pending sales, closed sales and home prices. Mortgage rates hit a 20 month low. The one cause for concern: inventory is not keeping up with demand.

• The number of closed sales were slightly higher than a year ago, and the number of pending sales (agreements that have been signed but not yet closed) made it the best January in 15 years.

• Home prices throughout King County continued to climb.

• Supply of inventory fell by double digits.

Eastside

High demand and low supply continued to boost home prices on the Eastside. While closed sales were up, pending sales were down. The median price of single family homes sold on the Eastside in January was $625,000, an increase of about 4 percent over last year. Inventory continued to drop to a two month supply. Areas close to the city centers experienced a particular shortage of homes for sale.

Seattle

Seattle continued to have the lowest supply of single family homes in King County. The city averaged 1.3 months of inventory, with northwest Seattle having just three weeks of supply. Low inventory pushed the median price of a single family home there to $517,500 – 13 percent higher than a year ago. The number of closed sales remained unchanged from a year ago, while pending sales were up slightly.

King County

The median price of single family homes sold in King County in January was up nearly 8 percent over last year to $441,500. Inventory continued to be very tight, with just a two month supply available. A supply of three to six months is considered balanced. With more consumers competing for less inventory, buyers should anticipate multiple offers for most new listings.

Read the original post on the Windermere Eastside blog.